RESILIENT GREATER CHRISTCHURCH PLAN:

Are you sick of hearing the word “resilience”? Has the word lost all meaning for you?

In June 2014, as part of the 100 Resilient Cities Network, a Chief Resilience Officer was appointed at council. For the following two years, the salary for the position was paid by the Rockefeller Foundation and almost nothing was heard of the activities the CRO was engaged in behind the scenes, despite the fact that the scheme purportedly “places people at the heart of a Resilient Greater Christchurch”. A further role of the position was to “address the needs of all city residents, and especially low-income and vulnerable populations, who were often hit hardest by shocks like natural disasters and chronic economic downturns.” Three years on, these groups are arguably in a worse position than they were in 2011 after the biggest natural disaster in New Zealand history, and council has repeatedly ignored pleas to help them (see below).

When interviewed on the subject of resilience in September 2016, for example, Mayor Dalziel was unable to give any concrete examples of what the CRO had actually achieved over the previous two years. Then, in September 2016, the mayor pledged 10% of funding in the 2017/2018 financial year for resilience projects, including the salary for the CRO. It is not clear what projects have been earmarked.

The following “Resilience Plan” from the Christchurch City Council has now become available, although, like the activities of the CRO, it has not been widely published. We believe it is an astonishing example of the total disconnect between theory, as trumpeted by the plan, and the actions and policies of the council in practice.

Alternative facts are on the march, so beware of the following terms as used in the document: resilience, vision, stakeholder, and engagement. These terms appear to be euphemisms for what the city council is actually planning, which, in many cases, is the exact opposite of the accepted meaning of the term (resilience = residents taking on and paying for risks; vision = plan to rid ourselves (councils) of liability; stakeholders/we/us = the authorities, not the ratepayers; engagement = spin and propaganda to convince people of alternative facts).

Click on the picture to read some of the key statements and statistics from the document, which has not been widely shared or publicised among the city’s worst affected communities. Empowered Christchurch comments are in italics following the excerpts.

“Resilience is a word we have heard a lot in Greater Christchurch over the past five years. No matter what extent to which [sic] we are familiar with this word in our day-to-day lives, it is important that we collectively understand the concept of resilience.

We know that we will encounter future challenges. This is not simply about preparing our infrastructure or our built environment and it’s not about bouncing back to the way things used to be. For us, resilience will be about understanding the risks and challenges we face and developing ways to adapt and co-create a new normal. The strength of our resilience lies in us, not just as individuals, but as communities and whānau.

The [PDF 8.8MB] enables us as city and district leaders to work together to enable and empower our communities to face the future with confidence. As a group of leaders we were already working together before the earthquakes struck.

The Urban Development Strategy (UDS) has as its vision:

By the year 2041, Greater Christchurch has a vibrant inner city, and suburban centres surrounded by thriving rural communities and towns connected by efficient and sustainable infrastructure. There are a wealth of public spaces ranging from bustling inner city streets to expansive open spaces and parks, which embrace natural systems, landscape and heritage.

Innovative businesses are welcome and can thrive supported by a wide range of attractive facilities and opportunities.

Prosperous communities can enjoy a variety of lifestyles in good health and safety, enriched by the diversity of cultures and the beautiful environment of Greater Christchurch.

The vision has not only survived our experience; it has been enhanced. We see this resilience plan as enabling the review of the strategy to occur with a resilience lens and an ongoing commitment from each of us to visible collaborative leadership.

As we shift from recovery to regeneration, we can restate the importance of collaboration; between the city, the districts and the region, Central Government, the Canterbury District Health Board and most importantly with the many and varied communities that make up this special part of New Zealand.”

“Our plan places people at the heart of a Resilient Greater Christchurch.” (Presumably, that is why this document has not been publicised among the affected communities or the general public.)

“Being resilient relies on understanding, preparing, coping and adapting to the threats we face.”

(For example, by ignoring the threat from climate change for decades; by circumventing legislation after the earthquakes to increase the risks for residents; how did the Council understand, prepare, cope and adapt to create the chaos that followed the November 2016 tsunami alert? It did not have, and in all likelihood still does not have, an efficient communication system or tsunami evacuation plan in place; warnings and notifications about the various threats from community groups have been ignored.)

“Chronic stresses for Greater Christchurch include climate change, affordable quality housing, psychosocial well-being and an aging population.”

(According to the plan’s statistics, 43% of housing in the eastern suburbs is in an “as is” condition following the earthquakes. This situation is largely the responsibility of the EQC, the Christchurch City Council and private insurers. Canterbury had a record 83 suicides in the last year, almost certainly due in part to the chronic stresses mentioned, which have been actively added to by the City Council. Many of the most vulnerable victims to chronic stresses are members of our elderly population.)

Brighton beach and the Brighton Peninsula are featured on the cover pages of the Resilience Plan.

These are the areas that have been most shamefully neglected by the Council, where 80% of the most socially deprived in Christchurch live, and where, as mentioned above, “as is” properties now comprise 43% of the housing stock. Complaints, arguments and notifications from the residents of these areas have been consistently ignored, even while the Christchurch City Council was developing this ‘resilience’ plan.)

Resilience is the capacity of individuals, communities, businesses and systems to survive, adapt and grow, no matter what chronic stresses and acute shocks they experience.

(Most of the chronic stresses and acute shocks that Christchurch residents have experienced stem from the incompetence of its elected representatives and their response to the earthquakes.)

| Hutia te rito o te harakeke, kei hea to komko e ko?Whakatairangatia, rere ki uta, rere ki tai.

Ki mai ki ahau, he aha te mea nui o tea o, Maku e ki atu: He tangata, he tangata, he tangata.

|

If we were to pull out the centre shoot of the flax plant, where would the bell bird sing from?It will fly aimlessly inland and out to sea.Ask me what is the most important thing in our world?

I will reply: It is people, it is people, it is people.

|

| Sir James Henare, Ngati Whatua, Nga Puhi nui tonu | |

P10: “Embracing participatory planning and collaborative decision-making.

Statistics

8000 households permanently displaced by land damage, 90% of residential properties damaged in some way, and 80% of buildings in the CBD have had to be demolished.

1,628,429 m² of roadwork damaged

659 km of sewer pipes

69 km of water mains damaged

Approx. 168,000 dwellings with an insurance claim

1100 buildings in the CBD had to be demolished

Recovery work

Waste water

583 km of pipe (88%) repaired/replaced

73 pump stations (90%) repaired/replaced

98% of total design work is complete

Storm water

59 km of pipe (83%) repaired/replaced

For pump stations (74%) repaired/replaced

93% of total construction is complete

Fresh water

96 km of pipe (98%) repaired/replaced

22 pump stations and reservoirs (81%) repaired/replaced

97% of central city work is complete

Roading

1,300,000 m² of road (94%) repaired/replaced

142 bridges/culverts (99%) repaired/replaced

158 retaining walls (87%) repaired/replaced

94% of the whole SCIRT programme is complete”

(Figures from July 2016)

P16 “Black Map” (An early map showing the many areas of swamp in the city in 1850. This is often used as an argument to ignore the effect of land settlement after the earthquakes?)

P18 “Ground subsidence caused by the recent earthquakes has elevated the severity and frequency of flooding events.” (And nothing has been done to remediate the subsidence or compensate residents pursuant to the Earthquake Commission Act.)

“… in the future it is likely to be coastal flooding, storm surges and inundation that are the greatest threat.” (Threats that Empowered Christchurch has repeatedly pointed out to the council over recent years without any response and action being taken.)

“Housing and social equity

Loss and damage to homes as a result of the 2011 earthquakes drove up rental prices, left people sleeping in garages and cars and contributed to an exodus of people from the region. It took major releases of land and rapid investment in housing over four years to resolve these effects.”

(This ignores the chronic condition of “as is” properties, and the slumification of the eastern suburbs that has been actively promoted by the council. Infrastructure has been removed and not replaced; homes have been built below the Building Act requirement; existing use rights have been granted for insurance rebuilds; council has failed to allocate donations to their specified recipients.)

P36 “Residents want to be involved in the decisions that affect their neighbourhoods and communities….

the shift in focus to regeneration offers an opportunity for a more deliberate and collaborative approach to decision-making.”

(There has been little sign of this happening.)

P49 “What outcomes do we expect to see?

Vulnerable people are well supported and participate in the community, which helps to decrease feelings of isolation and loneliness.”

(Up to now, it is the primarily the vulnerable members of society who have been targeted in the recovery: those with low incomes, older residents and the socially deprived.)

P51 “What outcomes do we expect to see?

Successful current examples other Activities include:

- Build Back Smarter

(Unfortunately, this initiative was not launched until February 2015 when most rebuilds/repairs had been completed. A total of 1400 homes received an assessment under the scheme, but only 53% made changes.)

“Ko te kai a te Rangatira he korero

Conversation is the food of chiefs”

(This clearly does not apply for the Mayor of Christchurch. Despite an assurance that we would receive a response, Empowered Christchurch is still waiting for a reply to our letter of 14 February 2017.)

P60 ” The challenge is to build more trusting relationships between communities and decision-makers in Greater Christchurch. Central to this is changing the way in which governance engages with people, as all too often their processes rely on rigid and formulaic methods that are set up to be adversarial… Transparent and participatory governance empowers the community.”

(Once again, we have seen no sea change in attitude in this regard. Council has adopted an adversarial attitude towards ratepayers.)

P66 Eastern Vision and its website EVO SPACE

(This is one example of the many pseudo-community consultation schemes that have sprung up since the earthquakes.

When it began in 2014, it was run by a former city councillor and funded by the Canterbury Earthquake Recovery Authority – CERA. The website is extremely basic, with just two pages, one entitled HOME, and one entitled RESOURCES. The Resources page consists of a video, a “doodle map” – a map of eastern Christchurch – for visitors (or perhaps their pre-school children) to draw on (!), and a link to request a workshop, with absolutely no information on what expertise the group possesses or can offer.)

LinC Project

A further example of stage-managed community engagement: this programme has provided training for two batches of 40 and 45 so-called “community leaders”. It is heavily influenced and directed by government and the authorities – 10 of the second batch of 45 candidates “selected” came from government organisations and one of its “facilitators” is now employed by Regenerate Christchurch, the successor to CERA. It appears as if these candidates are being groomed for positions in further pseudo-community organizations with the task of countering the current criticism from community representatives.)

P85 “What outcomes do we expect to see?

Open and transparent engagement with people using understandable information to help them make decisions and balance the consequences of action or inaction in relation to risk management.

(It is inaction in relation to risk management on the part of the authorities, and the city council in particular, that has exacerbated the said risks of flooding, inadequate housing, psychosocial stresses, etc.)

Successful current examples of activities include:

Dudley Creek and Flockton Basin Flood Mitigation Schemes

(Despite implementation of a $48 million drainage project, the Flockton area flooded in the recent rain following Cyclone Cook.)

P88: Risk Transfer

“The New Zealand Earthquake Commission (EQC) scheme underpins the availability of affordable insurance for residential property and assets in New Zealand. … 70% of losses from the major earthquake events of the Canterbury Earthquake Sequence were covered.”

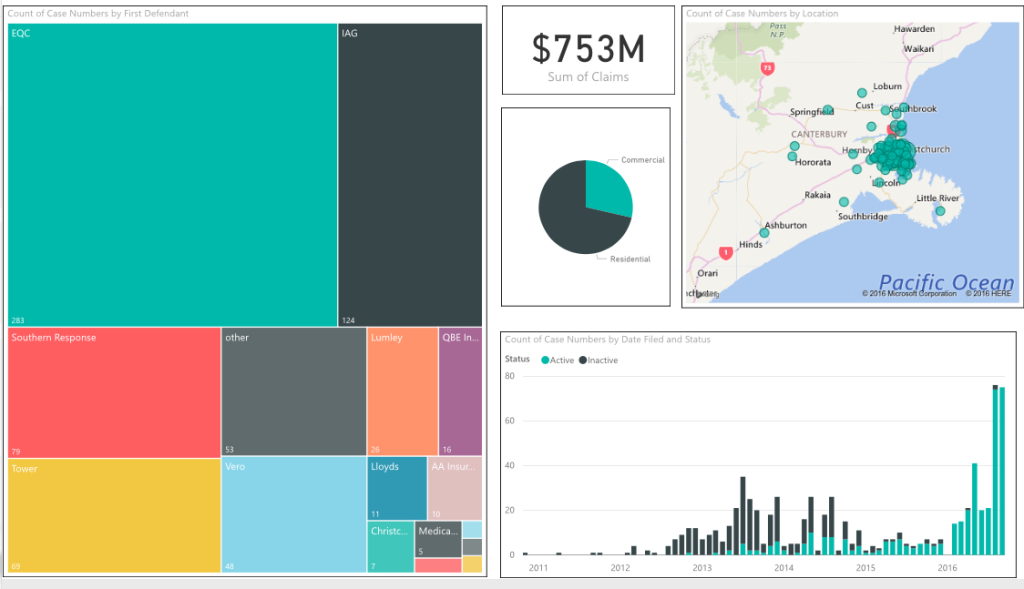

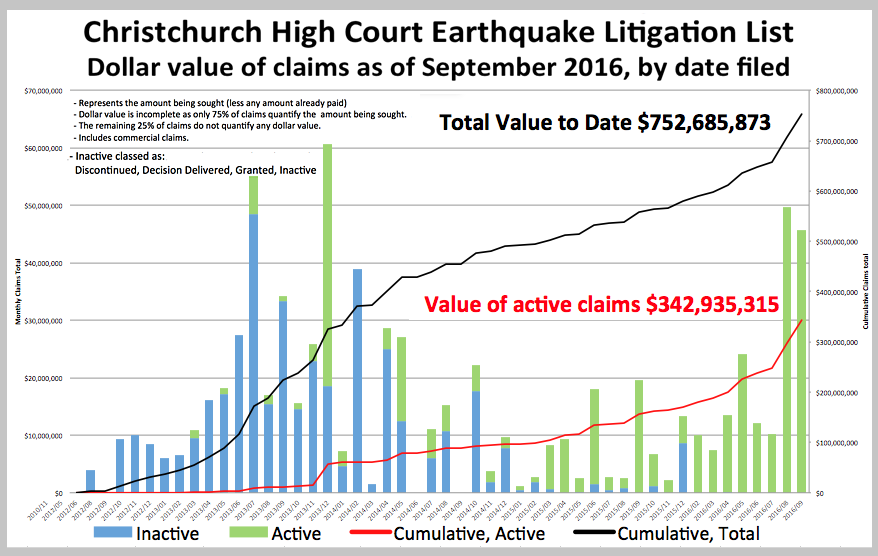

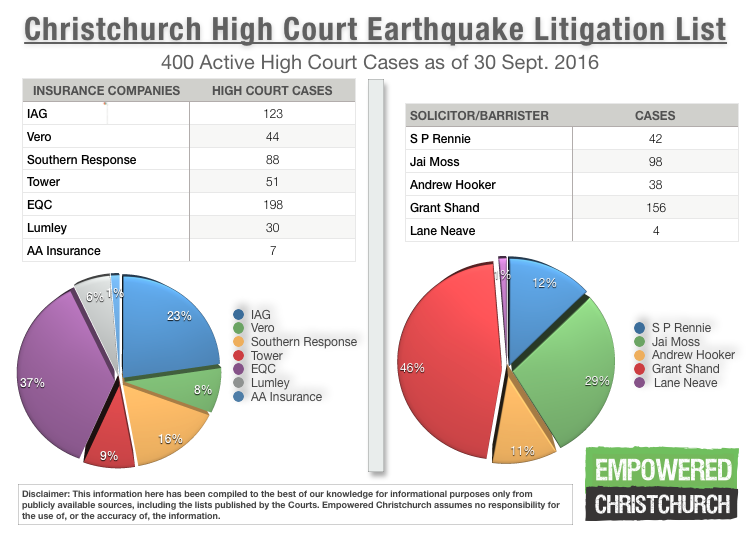

(The EQC is currently depending 199 earthquake litigation cases in the Christchurch High Court. It has been a signal failure in terms of its raison d’être – to protect the people of New Zealand against the effects of natural disasters and cover their losses.)

Risk acceptance is a state of being that influences the level of risk reduction and risk transfer, and ultimately the level of tiredness we are willing to investing and it can change as we use other responses.

(So are residents to be prepared to enter a “state of being” where they accept risks that the authorities have created and actually exacerbated?)

P89 Securing our future in the eastern parts of Christchurch

6.3 km2 red zoned and 7,300 homes purchased by government.

“Securing our future in the eastern parts of Christchurch will require a multi-party collaboration to resolve a range of different issues that include social and economic problems, future risk from climate change, particularly sea level rise, and the reuse of earthquake damaged land, and water management. Our response needs to consider the cost as well as the potential benefits for the community.

(There is no mention of the obligations to deal with the earthquake damage, provide flood protection and to try to undo the mistakes of the past, such as allowing brand new homes to be built 50cm below the Building Act minimum, failing to designate high flood hazard management areas until 97% of insurance claims had been setteled.)

“The future of Eastern Christchurch will be founded upon a clear understanding of the risks that the area faces and from there a participative process can best determine how hazards are managed, new prosperity is built and how existing and new communities are connected.”

(A participative process has been missing over the last six years. The process of endless discussions and engagement with communities purely for PR purposes has not been accompanied by any action on the said issues on the part of the authorities.)

| East (as defined on map) | Christchurch City | |

| Area population | 62,500 | (20%) |

| % Maori and Pacific populations | 29%/34% | 8%/3% |

| Number of most socially deprived people | 23,500 | 29,375 |

| Average house price | NZ$ 335,000 | NZ$ 445,000 |

| Households earning under NZ$ 100,000 | 84% | 73% |

| Households earning under NZ$ 50,000 | 48% | 38% |

| % Households renting their home | 43% | 35% |

| % Households drawing state financial support | 28.5% | 17% |

| Qualifications % without qualifications |

29% | 20% |

| % with university qualifications | 12% | 21% |

| % Households with Internet access | 70% | 79% |

P90 Land elevation map – Eastern Christchurch

(The red line indicates the statistical area of the quoted data. If this refers to the above statistics (and not just those following), the suburbs of South Brighton and Southshore have been excluded!)

Chief Resilience Officer statement

“Specific issues raised during the development of this plan recognized the need to build a more trusting relationship between communities and decision-makers, nurture existing community networks and support systems …

… underpinned by the need for strong and effective leadership.”

(Once again, all of the Council’s actions belie any serious interest in achieving this goal.)

***END

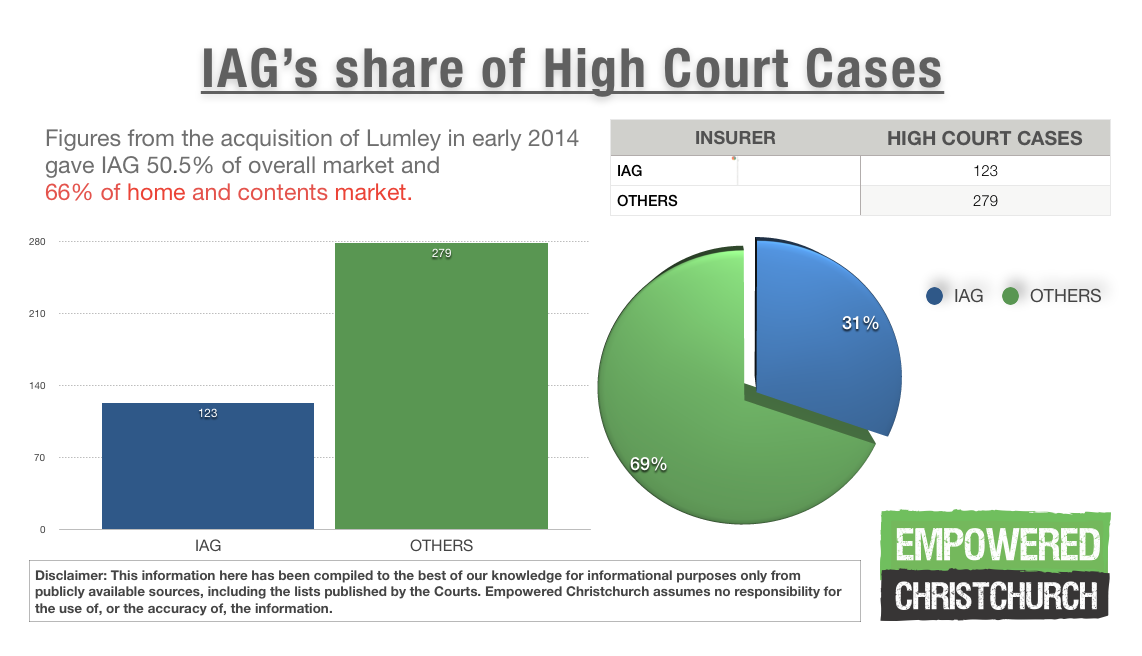

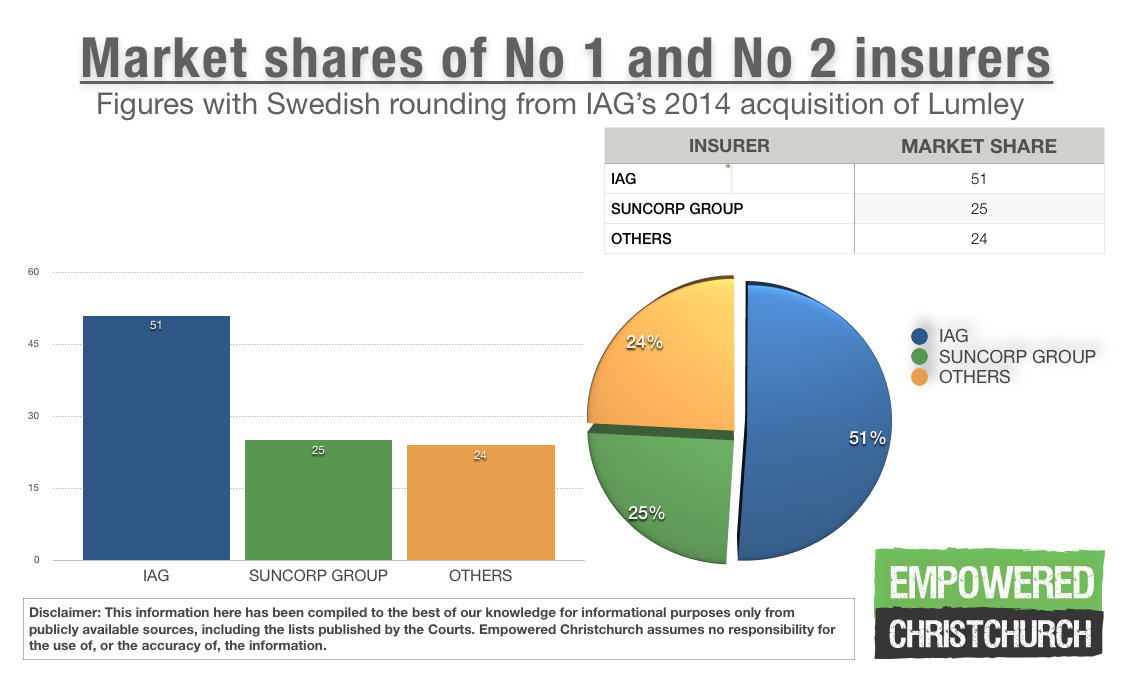

Figure 5: Market shares of IAG plus Suncorp

Figure 5: Market shares of IAG plus Suncorp