AN OPEN LETTER TO THE MINISTER OF JUSTICE

Appeal for access to justice for Canterbury earthquake claimants

“THERE ARE TWO LEGAL SYSTEMS: ONE FOR THE RICH AND POWERFUL, AND ONE FOR EVERYONE ELSE.”

(Elizabeth Warren, US Senator for Massachusetts, 2016)

Dear Minister

You recently gave a speech at the Law Foundation Awards Dinner in Wellington on improving access to justice. Your comments focused mainly on criminal law, but you also mentioned in passing that many rights are not enforced because of the cost of pursuing civil claims in the courts. As the coalition government works to find ways to resolve the remaining claims, we would like to examine some of the obstacles to justice for earthquake claimants in Canterbury, discuss how these obstacles could be removed, and consider the long-term consequences for New Zealand as a whole from the Canterbury earthquake recovery.

PART A: Obstacles for claimants:

1) The adversarial system

In March 2016, Justice Stephen Kós, who is one of the Earthquake List judges, outlined some of the shortcomings of the New Zealand legal system and the difficulty in gaining access to justice[1]. He pointed out that New Zealand was ranked in ninth place in the World Justice Project Rule of Law Index metric for civil justice, and that all of the countries above it (bar one – Singapore) were civil law countries with more inquisitorial systems of civil justice. He went on to contrast the objective of the latter systems, namely the “revelation of the truth”, with the adversarial system, which is “not necessarily concerned with the identification of truth”.

The government is now looking to establish an earthquake tribunal, but no information has yet been released about what format this might take or what legislative changes would be required. Up until now, the process of suing the Crown entity EQC, the government-owned Southern Response, or a private insurer for an earthquake claim has been a long and protracted one. Apart from legal professionals, the claimant needs to engage the services of at least four different experts: a professional surveyor, a structural engineer, a geotechnical engineer, and a quantity surveyor. The onus is also on the claimant to prove their loss. In practice, this means that the defendant is able to make extravagant claims, which must then be disproved by the plaintiff. By way of example: the Christchurch High Court heard one case where the defendant claimed that damage to a house was caused, not by an earthquake, but by wind or by a flax bush[2]. In many earthquake cases, the more serious underlying problem is land damage, which both the Earthquake Commission and private insurers have made strenuous efforts to avoid addressing. Many “as-is” properties have been sold that are on land at high risk from erosion or flooding as the result of earthquake subsidence. Empowered Christchurch has repeatedly emphasized the importance of determining the condition of land and the damage that has occurred to it before either repairing or rebuilding homes. This was rendered impossible in the rebuild because the EQC only began to compensate claimants for land damage in 2015. The full facts about how badly some areas of land have been affected are only emerging now, with the government’s focus on climate change, and the acknowledgement that parts of Christchurch experienced the equivalent of 80 years of sea level rise in terms of the risks from flooding and erosion.

The High Court Declaratory Judgement in December 2014 involved two intervenors on behalf of residents, and two amici curiae. However, there was no representation for coastal residents, who have been worst affected by the EQC approach of making diminution in value payments without either mitigating or eliminating the risks posed by flooding and liquefaction. Many claimants who have received DoV payments for increased flooding vulnerability may lose access to insurance cover in the future if their properties experience repeated flooding.

2) Hearing charges in the High Court

A substantial number of earthquake claimants cash settled with their insurers simply because they could not afford the cost of High Court litigation.

Low-income and vulnerable earthquake claimants are seriously disadvantaged in the New Zealand justice system. A private individual must meet costs for lawyers and solicitors, expert reports and filing charges, with no prospect of reimbursement of even part of these costs until a final decision is reached in court.

A further obstacle is hearing fees: these are currently $3,200 per day in the High Court, $2,700 per day in the Appeal Court, and $1,000 per day in the Supreme Court.

In 2013, the New Zealand Law Society argued against the increase to the fees at that time: “High Court fees for these proceedings should remain unchanged. It should not be forgotten that the judiciary are the third branch of government. The public is entitled to have access to the courts as a fundamental part of our constitutional structure. Fees that create barriers to access are arguably unconstitutional.”[3] The fee increase was also criticized as being revenue-driven on the part of the government, but was nevertheless implemented.

Other systems for defraying plaintiff costs, such as litigation funding and class actions, are still in the development stages in New Zealand, and subject to various rules and regulations. On this subject, the New Zealand Law Society quotes Liesle Theron, a litigation partner at Meredith Connell: “Access to justice is repeatedly identified as a critical issue for the profession. I see group litigation and litigation funding, separately and in combination, as powerful tools that can provide part of the solution”.[4] Facilitating these options would also help to redress the balance.

3) Court procedures

After waiting for periods of up to 2 years and more for a date in court, a number of earthquake cases have been adjourned because insufficient time was allocated to hear the evidence.

Adjournments can mean a further delay of up to 9 months. This further obstacle could be avoided if a minimum period of, say, 12-15 days, was allocated to hear each case. If cases are concluded in a shorter period, other cases can be brought forward.

Of the 45 High Court judges available, only a small number (8 since the “fast-track” system was established) have been assigned to hear earthquake list cases, and the vast majority of cases so far have been heard by just three judges.

Conflicting expert reports are often provided by the defendants and by the plaintiffs. However, many of the reports submitted by the defendants in earthquake cases contain waivers, asserting that the authors take no liability for the contents of the report. This should render the report useless as evidence, since the essential purpose of a structural engineering report or geotechnical report is to provide a foundation solution for the repair or rebuild of a particular building. If the author takes no responsibility for the content of the report, its proposals cannot be relied on for the actual building project in question.

A further obstacle for claimants is that insurance companies have recently attempted to exclude professional surveyors from joint expert meetings[5].

As mentioned above, this excludes consideration of land damage. Compliance with Building Code sections E1 and E2, Flood Management Area requirements, drainage design, secondary flow paths, and flood resistance are consequently all omitted from the evidence. These aspects are of critical importance for the proposed solutions from structural engineers and geotechnical engineers.

The principle of judicial impartiality needs to be strictly observed. To avoid any appearance of a conflict of interest, judges who serve in the High Court earthquake litigation list should have no association with the defendants (the Crown entity EQC, the government-owned Southern Response, or private insurance companies) to avoid any conflict of interest. For example, judges who have previously served as Crown prosecutors should not be hearing cases where a Crown entity or Crown-owned company is the defendant.

4) Limitation period and excessively long waiting periods

− “Justice delayed is justice denied”

After seven years, the Earthquake Commission is still transferring claims to private insurers. The total number of unsettled over cap claims was 2,912 as at the end of June 2017. A number of private insurers are now starting to use the limitation period to deny their liability. This is a shameful abandonment of both their responsibility to policyholders and their liability for earthquake claims. The reason for the seven-year delay in settling claims has been a process of delay on the part of the EQC and private insurers, rather than claimants. In 2016, Empowered Christchurch appealed to the then Minister of Justice, Amy Adams, to extend the limitation period for earthquake claims. Our request was declined. In view of the fact that many of the delays stem from misinformation and/or incompetence on the part of government ministries[6], in the past, we believe there is a strong argument for extending the limitation period as we requested last year.

Even those insurance claimants who have filed proceedings have seen their resources drained over a number of years. The more protracted the waiting period, the more heavily the scales of justice are weighted in favour of insurance companies with deep pockets and massive resources. The “fast-track” approach for earthquake claims that was set up in 2012 by your predecessor, Minister Judith Collins, currently involves waiting up to 18 months on average between filing and obtaining a date in court. General proceedings take an average of 381 days to conclude.[7] One claimant reportedly has been waiting for more than 2 years since filing and has still to obtain a court date.

The substantial legal fees involved have driven some despairing claimants to represent themselves when taking their case to the High Court, a procedure that is fraught with risk for private individuals with no experience of the complexity of regulations and procedures.

5) Low income/low-education/vulnerable claimants

Many claimants are overwhelmed by the mass and range of technical detail and jargon involved, which ranges from the provisions of their insurance contract to the various expert reports and legal correspondence. Elderly people living alone are especially affected by this and are more likely to be pressured to cash settle by their insurance company. Claimants have been subjected to mental, emotional and economic pressure and this is reflected in the increased statistics from the Canterbury District Health Board and social services for family violence, divorce, mental illness and suicides (see below).

PART B Consequences for New Zealand from the obstacles to access to justice in Canterbury

1) Long-term social costs (health, mental health)

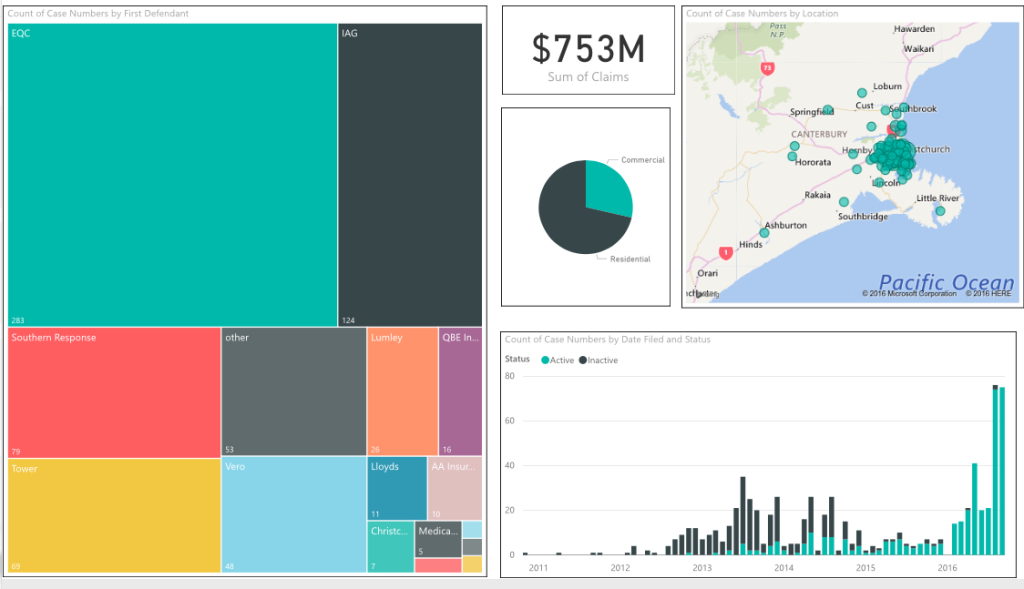

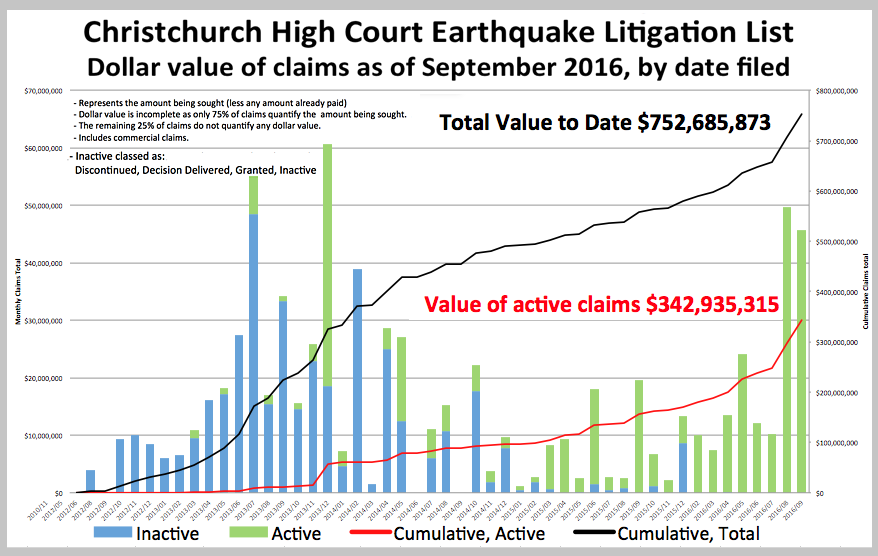

Despite the relatively small number of claimants who have litigated, more than $1 billion is currently being claimed in the Christchurch High Court. A large number of additional claims are expected in the New Year, in particular against the EQC for failed repairs and so-called “diminution of value” settlements for land damage from subsidence and liquefaction. The seven and a half years since the first earthquake have seen a steady increase in the amount of earthquake litigation and the work for judges, barristers and solicitors, but the protracted procedure involved is costing the New Zealand economy. Aside from the excessive burden it places on the justice system, and the energy and resources being devoted to earthquake litigation that could more usefully have been deployed elsewhere, there are long-term costs for society that will only become fully apparent in the years to come. These include duplicated effort and expense for failed repairs (in many cases tax payers’ money through EQC activities), short-term solutions for housing and infrastructure that will have to be revisited, the health and social services costs mentioned above, insurability issues, and missed days of employment.

We believe the impact on health is one aspect of the Canterbury earthquake recovery that has not received enough attention. In the last year reported, the region saw 76 suicides, almost twice the figure in Waitemata, an Auckland health district with a roughly similar population to Canterbury. Over the same period, there were 2,800 police callouts in Canterbury because of attempted suicides. A local health practitioner, in a submission to the Christchurch Annual Plan in 2017, described a spike in referrals in the eastern suburbs for mental health counselling. It is more than likely that there is a correlation between these figures and the poor quality of life, substandard housing and the mental, emotional and financial pressures many people have been exposed to in pursuit of a fair insurance settlement.

2) Loss of faith in government, the justice system and the insurance industry

The previous government has been responsible for many of the complexities and delays in the search for justice following the Canterbury earthquakes.

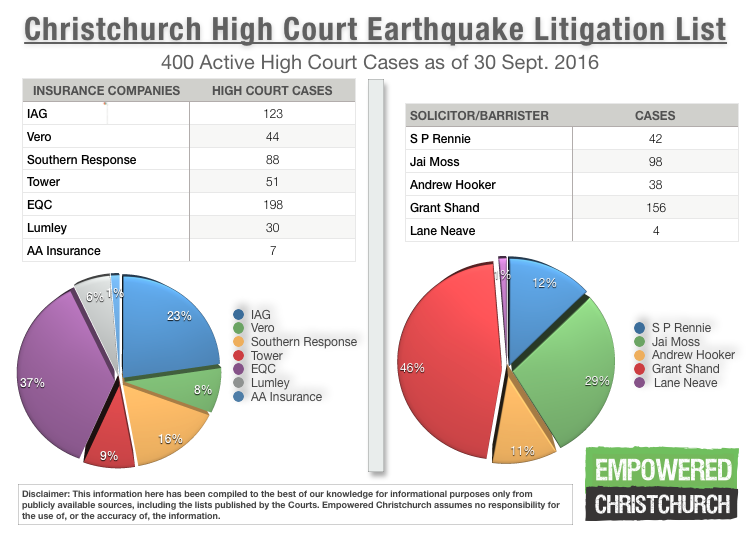

Claimants see themselves pitted against the forces of central and local government, allied to the insurance industry. Against such formidable opposition, they ask themselves if is there any chance of justice. Securing competent and effective legal representation has also been a challenge for many. A number of litigation cases have foundered on the rocks of legal incompetence and poor preparation. A very small number of modest law practices represent the bulk of earthquake claimants. Insurers and the Crown defendants, on the other hand, are represented by the biggest and most expensive law practices in the country. So the question is: can individual claimants have faith in the justice system?

Various organisations have emerged over the last five years with the purported aim of advising or advocating for earthquake insurance claimants. The most prominent example is the Residential Advisory Service (RAS), which at its launch received $325,000 from New Zealand insurers, immediately signalling that its role would be as an advocacy service for insurance companies to reduce the number of cases going to court. The fact that this organisation was heavily promoted and funded by central and local government and private insurers did not and does not inspire a great deal of trust, and a number of Canterbury earthquake claimants have stated that consulting the service proved an inordinate waste of time. The service is now controlled by a government ministry (MBIE, which also produced guidelines that have been used to circumvent the standards in the EQC Act and in private insurance contracts, thereby denying thousands of claimants repairs and rebuilds of the proper quality, and saving the government and private insurers many millions of dollars). It is therefore concerning to learn that the government recently decided to provide RAS with an additional $700,000 in funding. Since the Earthquake Commission and Southern Response, two of the leading defendants in the earthquake litigation list, are a Crown entity and a government-owned insurer respectively, this is tantamount to a judge providing assistance to the defendant in a trial. The “arms length” principle applied to business transactions is of even greater importance in a judicial context. In essence, the government is using taxpayers’ money to fund an organisation dedicated to steering claimants away from litigating against the government itself.

Conclusion:

We believe the most immediate steps that the government could take to resolve the outstanding earthquake claims are as follows:

- Extend the limitation period for earthquake cases (only) to give claimants improved access to justice and the opportunity to pursue their claims in the courts

- Assign additional judges to deal with the growing backlog of earthquake list claims

- Apply a minimum period of 12−15 days for each claim

- Ensure that land information and reports from professional surveyors are included as evidence, both to ensure compliance with the Building Code and to address land issues such as subsidence, erosion and increased flood risk

- Reduce High Court hearing charges, and increase the threshold for legal aid for individual claimants

- Withdraw funding for the Residents’ Advisory Service or establish a service that is genuinely independent of government and insurers

- Amend current regulations to facilitate litigation funding and group/class actions

Kind regards

Empowered Christchurch Inc.

[1] Address to the Arbitrators’ & Mediators’ Institute of New Zealand and International Academy of Mediators Conference

[2] https://www.radionz.co.nz/news/national/255745/house-damage-blamed-on-wind,-flax.

[3] https://www.youtube.com/watch?v=3M80qVP3Lrg

[4] https://www.lawsociety.org.nz/news-and-communications/latest-news/news/seven-litigation-funding-services-in-nz

[5]https://forms.justice.govt.nz/search/Documents/pdf/jdo/32/alfresco/service/api/node/content/workspace/SpacesStore/2671ab4a-95eb-427f-b391-9ef4495ea439/2671ab4a-95eb-427f-b391-9ef4495ea439.pdf)

[6] MBIE guidelines, for example, which fall well short of insurance policy entitlement; inadequate insurance scopes based on the latter; lack of guidance from ministries on the applicable standards; delays from relying on advisory and advocacy services funded by insurers government, etc., etc.

[7] http://www.otago.ac.nz/legal-issues/research/otago642539.html

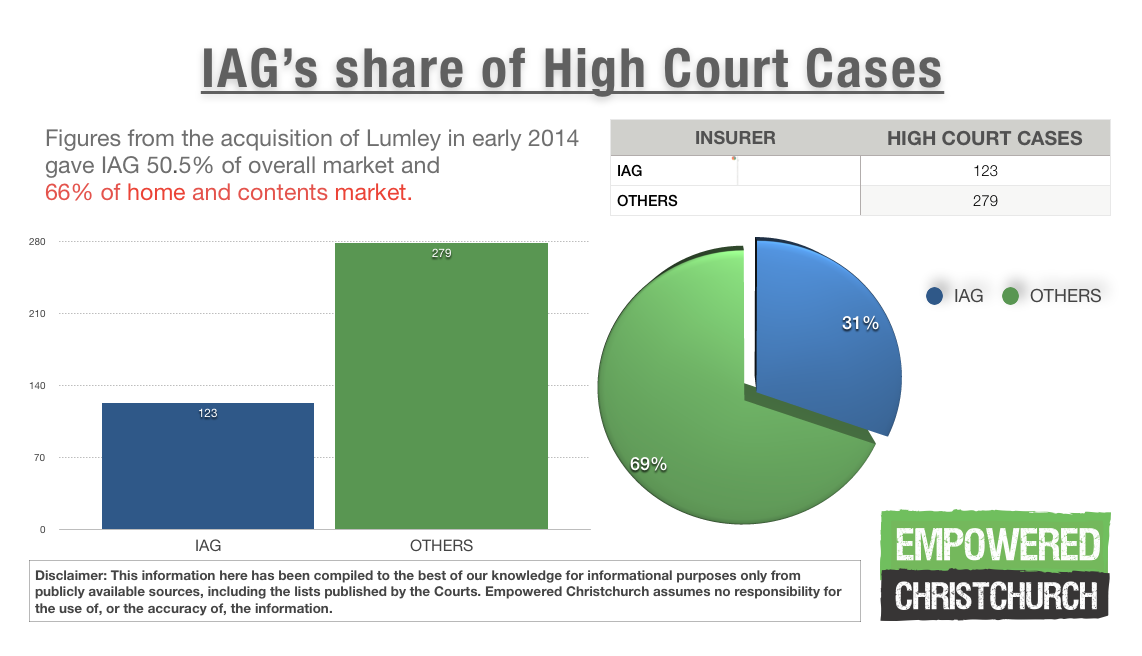

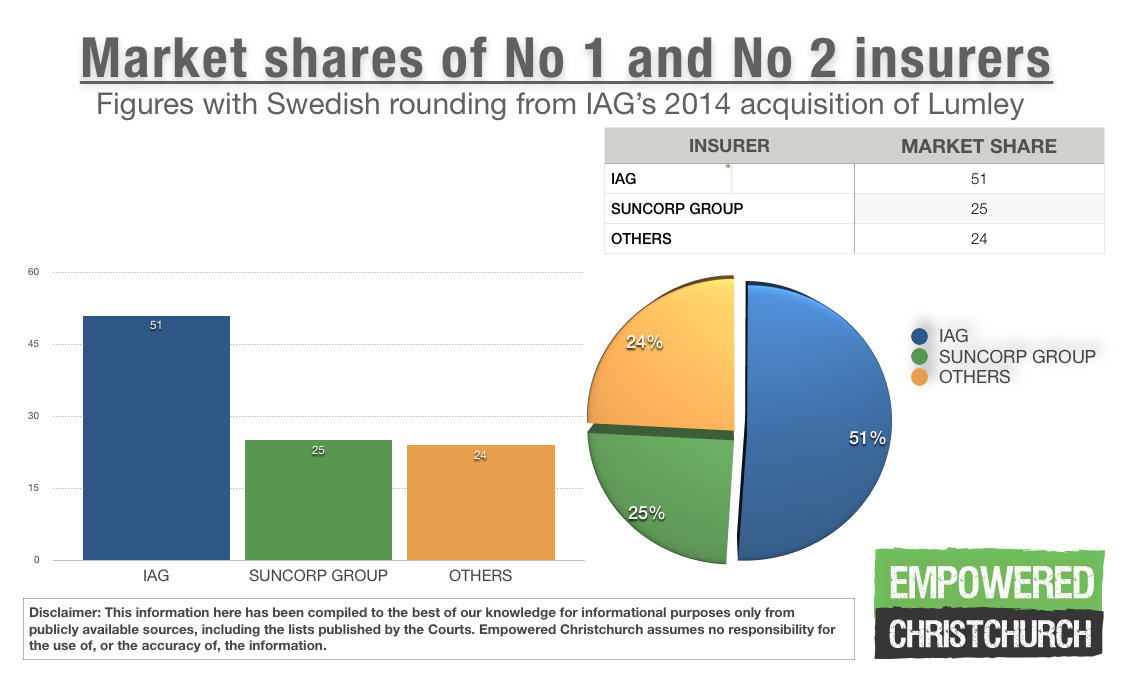

Figure 5: Market shares of IAG plus Suncorp

Figure 5: Market shares of IAG plus Suncorp